Q2 GDP Surges, But, But, But

Preliminary Q2 GDP came in at +4.1% this morning, right in the middle of my range. While the majority “expected” this accelerating growth, that was only in recent history, meaning everyone ramped up their forecasts lately. As I saw the number print, I thought that there would be no way for the naysayers and negative media folks to spin this against the strength that it is. But yes, they surprised me again with a chorus of “yeah, but”.

I heard that corporations pulled forward their buying because of tariffs. I heard that it was mostly because of soybeans. I heard that it was because the government spent much more money than expected. The bottom line is that 4% GDP growth is the highest in four years and fits in very nicely with my own bullish economic forecast for 2018 and into early 2019. It isn’t until mid-2019 to mid-2020 where I begin to have some concerns.

With the expected good news, I wouldn’t be surprised if bonds actually rallied where intuitively you would expect lower prices on economic strength. Bonds had been selling off over the past two weeks. Conversely, with stocks rallying nicely into the report, I would be surprised if we saw a big rally on Friday. In fact, the model of the day would be to use any early surge as a short-term selling opportunity.

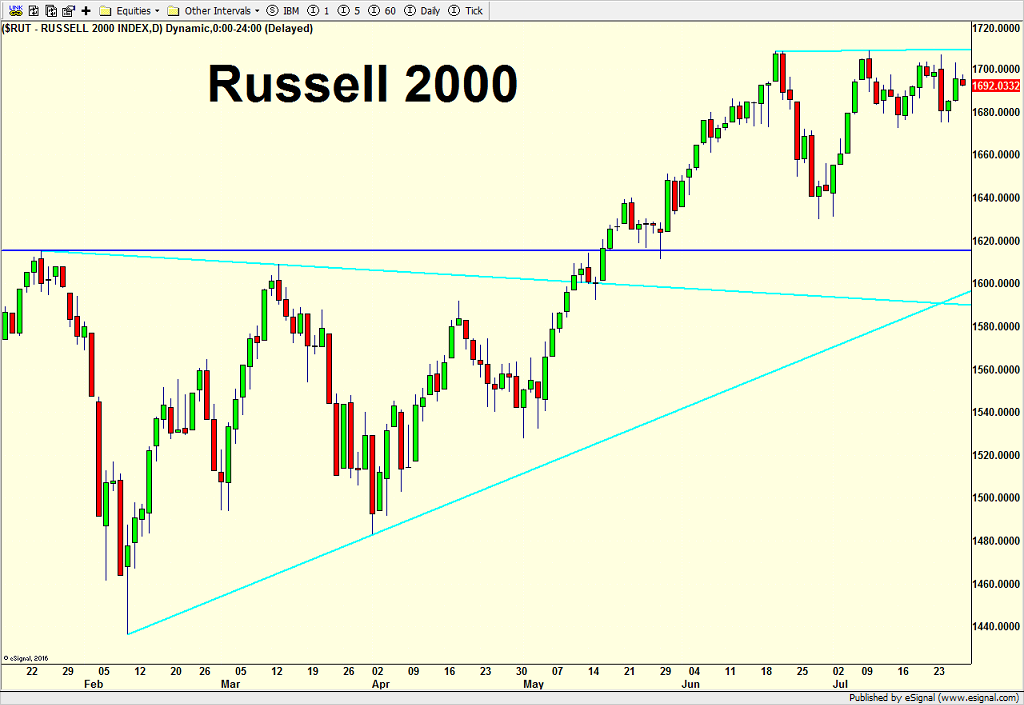

Looking at the major indices, there are no changes. I continue to favor the Dow Industrials and NASDAQ 100 over the S&P 400 and Russell 2000. Semiconductors have really woken up while banks and transports remain neutral. Discretionary is still the leader of the leaders. Junk bonds are continuing their quiet rally and the NYSE A/D Line forges ahead day after day to more all-time highs.