The Disaster That is GE with 3 Alternatives

Last week, I had the pleasure of joining the Nightly Business Report hosted by two CNBC veterans, Sue Herera and Tyler Mathisen. You can find the segment at the 22 minute mark HERE. This is one show I always enjoy as I am the only guest in the segment and they let me articulate my point. On this particular evening, GE’s dividend cut was the big story of the day and that spilled over into dividend paying stocks in general.

Before I continue, long time readers know I rarely spend much time discussing specific companies unless they are true bellwethers and I think there is a tie or correlation to the stock market. This piece is obviously different from most and if interested, please do your own due diligence.

For all of this century I have taken the negative (bearish) side whenever interviewed regarding GE. It had become an old, stodgy company whose best days were clearly far behind. When Jeff Immelt succeeded “Neutron” Jack Welch, that was the straw that broke the camel’s back. While I thought Welch needed a lesson in ethics and morality, I never thought Immelt was even competent to hold that much coveted position. Welch delivered results which is probably why no one targeted him, while Immelt was a complete failure.

Anyway, except for buying GE bonds for some conservative clients in 2009, I have pretty much avoided the stock altogether. There were always better opportunities elsewhere. Earlier this year, Jeff Immelt retired as CEO and subsequently left the board of GE last month. His successor is John Flannery. Flannery has been unusually candid and blunt about GE’s troubles, including its cash flow. As everyone knows, GE cut its dividend by 50% and I believe that’s only the third dividend cut in the company’s history.

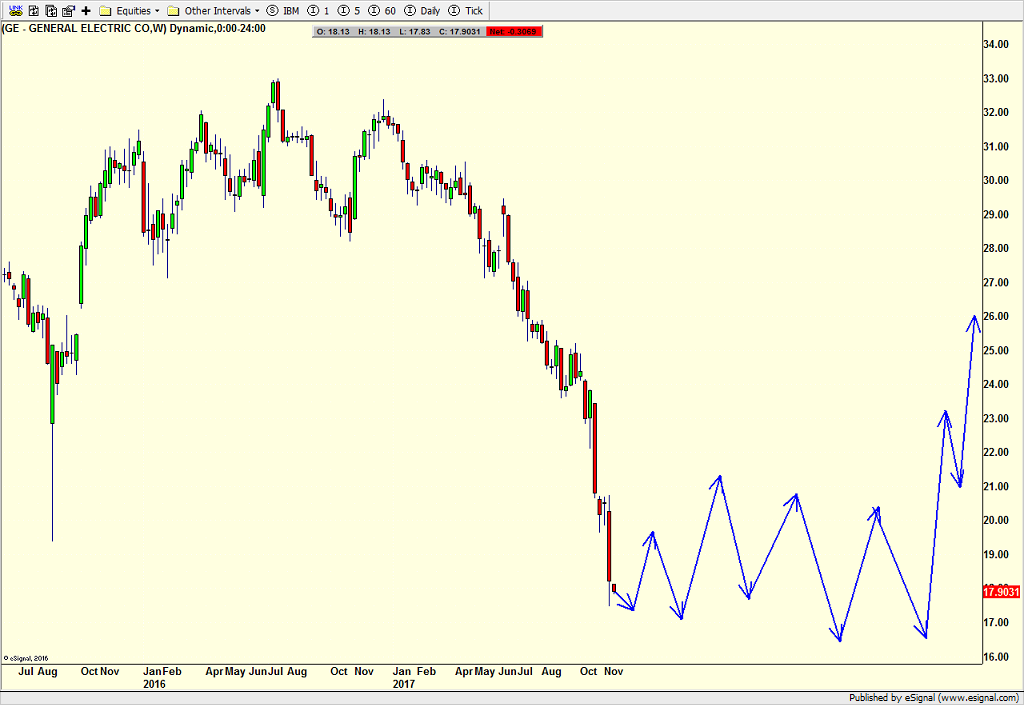

The dividend cut was a surprise to no one. Then Flannery pre-announced weaker earnings along with his turnaround plan. I thought investors would be a little comforted by this, but the magnitude of the decline in the stock after the news took me by surprise. The stock experienced a capitulatory, mini-crash on insanely high volume as you can see below.

When there are major shakeups at companies, new management often does a “kitchen sink” quarter where get all of the bad news out and then some. Anything that could possibly go wrong, they disclose, warn about and blame their predecessors. Then when everything doesn’t go as bad as forecast, new management gets to be the hero. In GE’s case, it almost feels like a “kitchen sink” year coming in up 2018.

GE has plenty of problems and then some. While I applaud Flannery for announcing a plan in the first place, he has his work cut out for him. And investors are not convinced. One of my close friends who runs a value fund boldly said to “stay away” as GE’s pension liabilities are overwhelming. On the flip side, one my colleagues just started nibbling on the stock with a plan to add more over time.

My view is that stock collapses like this are not repaired overnight. They usually take months or quarters and sometimes years to settle down and stabilize. Once a bottom (notice I did not say THE bottom) is reached, a stock usually enters a volatile and intermediate to long-term trading range where the bulls and bears battle around an equilibrium point until the light at the end of the tunnel is seen. In GE’s case, it could be in the mid teens to low 20s for a long time to come as you can see one potential scenario below. For the nimble traders, buying weakness and selling strength may be a good strategy until proven otherwise.

I don’t believe GE is a bellwether for the stock market, the dividend paying sector or large/mega cap value stocks. GE has its own idiosyncratic issues. Two ways to spot potential dividend cuts are to first watch how the stock trades. Sustainable dividend companies usually do not look like me skiing downhill on the weekends. That would be fast at a 25 to 40 degree pitch. Additionally, investors can track what’s called the Payout Ratio which is nothing more than the dividend of stock divided by the earnings. The higher the Payout Ration, the harder it is to sustain. While there is no hard and fast rule, especially when it comes to utility companies, 50% or less is an okay line in the sand. For all of 2017, GE’s stock warned and warned until the company listened.

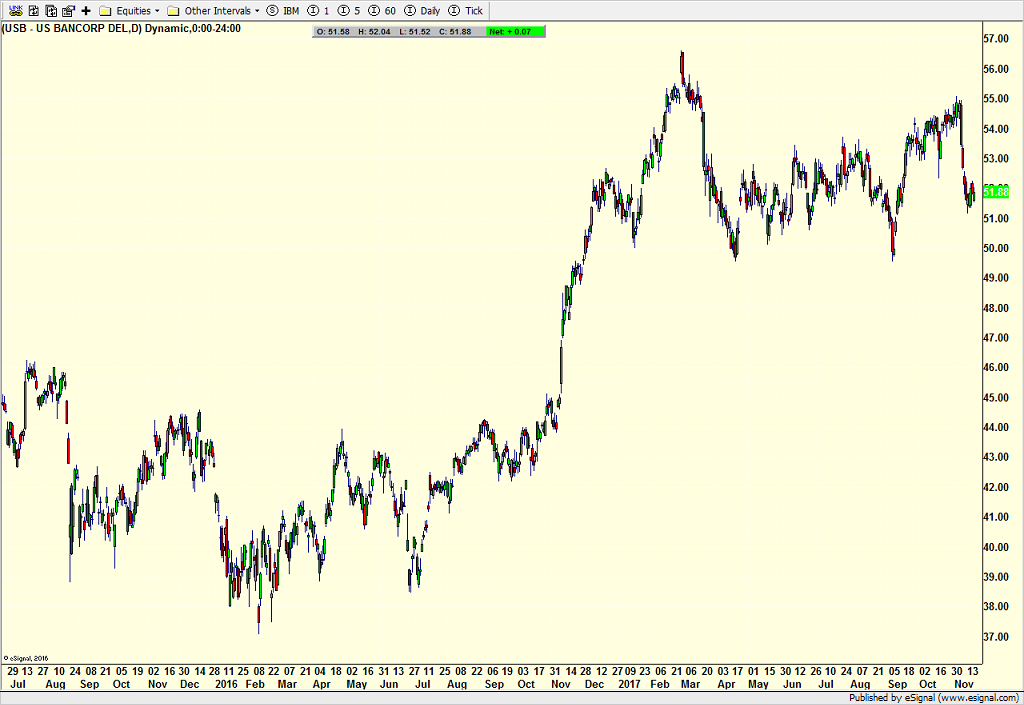

At the end of Nightly Business Report segment, I tried to squeeze in three dividend stocks which look attractive. US Bank, Pfizer and Brinker (owner of Chili’s restaurants) which yield 2.3%, 3.6% and 4.3% respectively. All three have Payout Ratios under 50%. None look like a ski slope although Brinker certainly saw its collapse and now appears to be emerging from the ruins as GE has a chance to do down the road.

US Bank looks to be under reporting earnings which may seem counter intuitive. As my colleague Jim says, they appear to be reserving too much for bad loans which don’t seem to be coming to fruition. Eventually, that money will manifest itself in higher earnings.

Pfizer, unlike many other large pharma companies, has no major drug coming off patent so there is no “fiscal cliff” on the horizon. The company is in an excellent capital position and the value may be in the individual assets, either in a spin off or sale to fully recognize their more cutting edge divisions in biotech. For full disclosure, certain clients own this company.

Brinker which fell on hard times as the casual dining sector has really slowed is a cash machine with a price to earnings ratio of only 13. Although the P/E can always get even cheaper, that’s a good value with that high dividend. The company could be appetizing as a buyout candidate or . For full disclosure, certain clients own this company.

As always, please do your own homework and/or consult your financial advisor. Don’t just take my word. Managing the downside is key and you absolutely need a plan if things don’t go your way. Riding any stock to oblivion isn’t a plan.

If you would like to be notified by email when a new post is made here, please sign up HERE